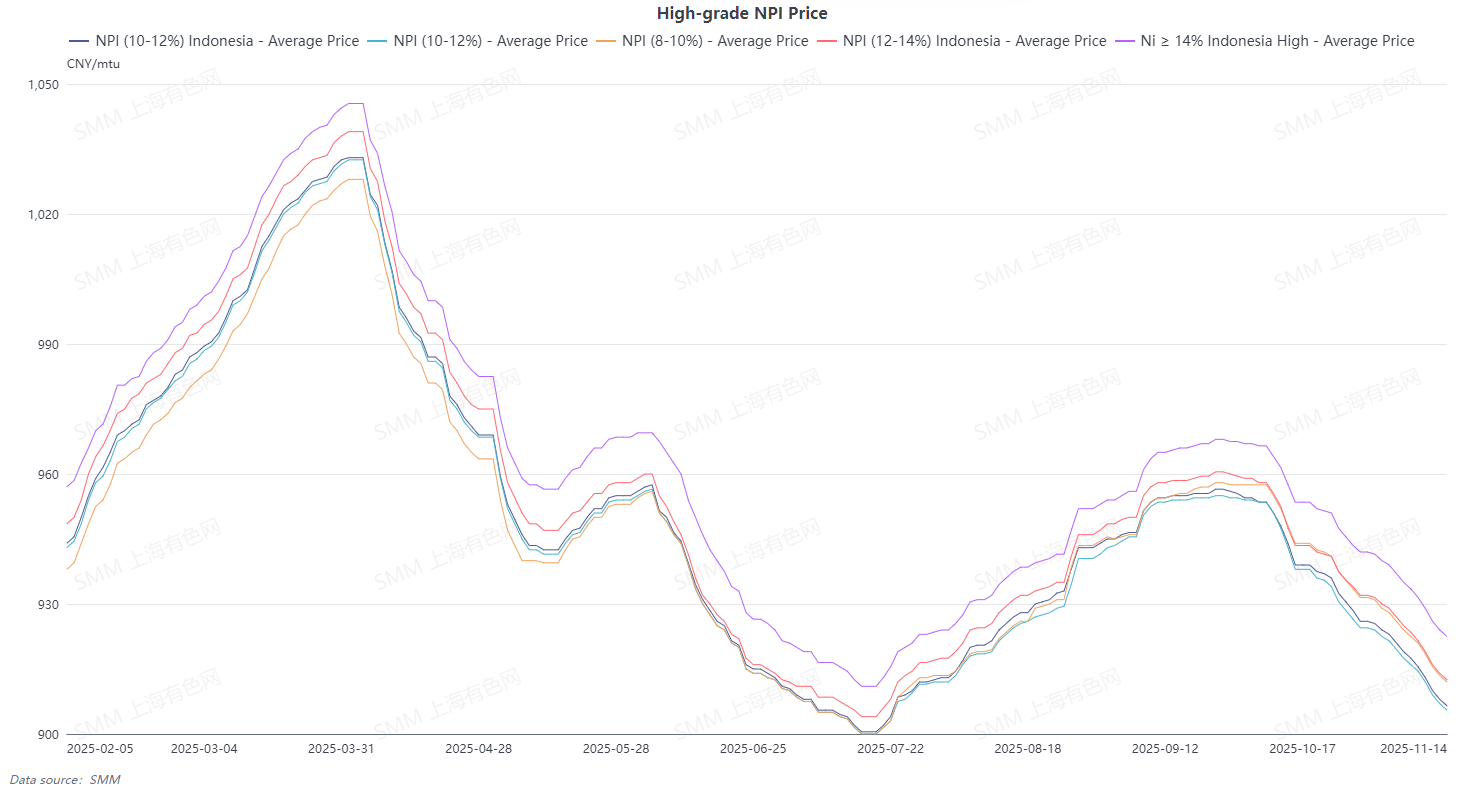

El precio promedio del NPI de alto grado SMM 10-12% cayó 9.8 yuanes/mtu en la semana a 909.6 yuanes/mtu (precio de fábrica, impuestos incluidos), mientras que el precio promedio del índice FOB del NPI indonesio bajó 1.1 dólares/mtu semanalmente a 112.37 dólares/mtu. Durante la temporada baja tradicional, el consumo final se mantuvo débil y los precios del NPI de alto grado continuaron disminuyendo esta semana.

En el lado de la oferta, a medida que los precios se acercaban a mínimos históricos, los fundidores aguas arriba aún se abstuvieron de ofrecer cotizaciones y los pedidos al contado registraron casi ningún volumen de operaciones. Sin embargo, en medio de un sentimiento bajista en el mercado, algunos comerciantes continuaron reduciendo precios para liquidar inventarios, lo que llevó a una mayor disminución tanto en las ofertas del mercado como en el centro de negociación.

En el lado de la demanda, con el inicio de la temporada baja tradicional, el consumo final se ha debilitado, las ventas de acero inoxidable aguas abajo enfrentaron una presión creciente y los márgenes de beneficio se redujeron aún más. Mientras tanto, los precios de la chatarra de acero inoxidable también continuaron retrocediendo. Ante los altos niveles de inventario y la creciente ventaja de costos de la chatarra de acero inoxidable, las empresas aguas abajo adoptaron un enfoque de compra más cauteloso, con un fuerte sentimiento de esperar y ver, reduciendo aún más el volumen de negociación del mercado.

En general, el mercado de NPI de alto grado experimentó una oferta y demanda débiles esta semana. El inventario total de NPI de alto grado en todos los segmentos aumentó mensualmente, la situación de exceso de oferta persistió y, sin una guía clara del mercado, se espera que los precios del NPI de alto grado permanezcan bajo presión.

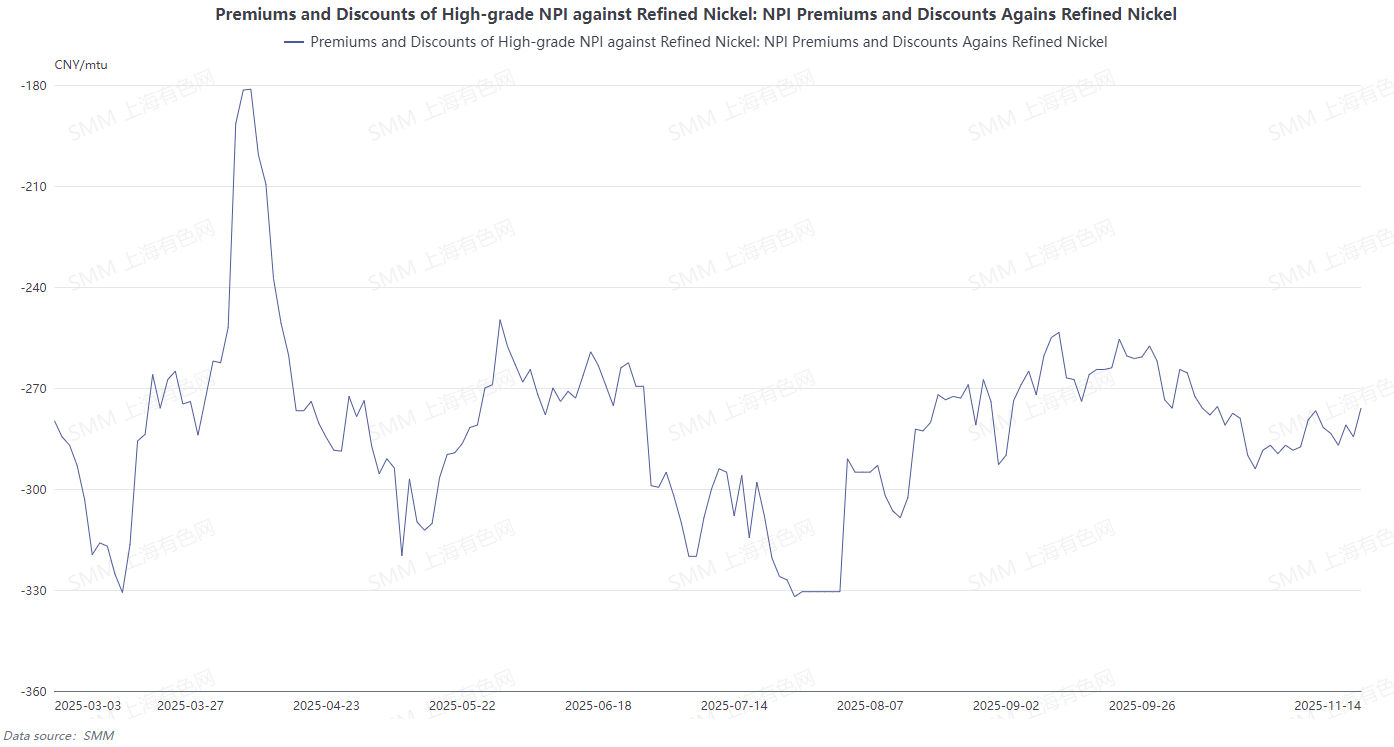

Esta semana, tanto el precio promedio del níquel refinado como del NPI de alto grado disminuyeron, con el descuento promedio del NPI de alto grado frente al níquel refinado reduciéndose ligeramente a 282.4 yuanes/tonelada. Se espera que los precios del NPI de alto grado sigan bajo presión la próxima semana, mientras que los precios del níquel refinado también probablemente permanecerán deprimidos. Se anticipa que el descuento promedio del NPI de alto grado frente al níquel refinado se expanda mensualmente, y se proyecta que el volumen de NPI de alto grado convertido a mata de níquel de alto grado se mantenga estable en comparación con el mes anterior.

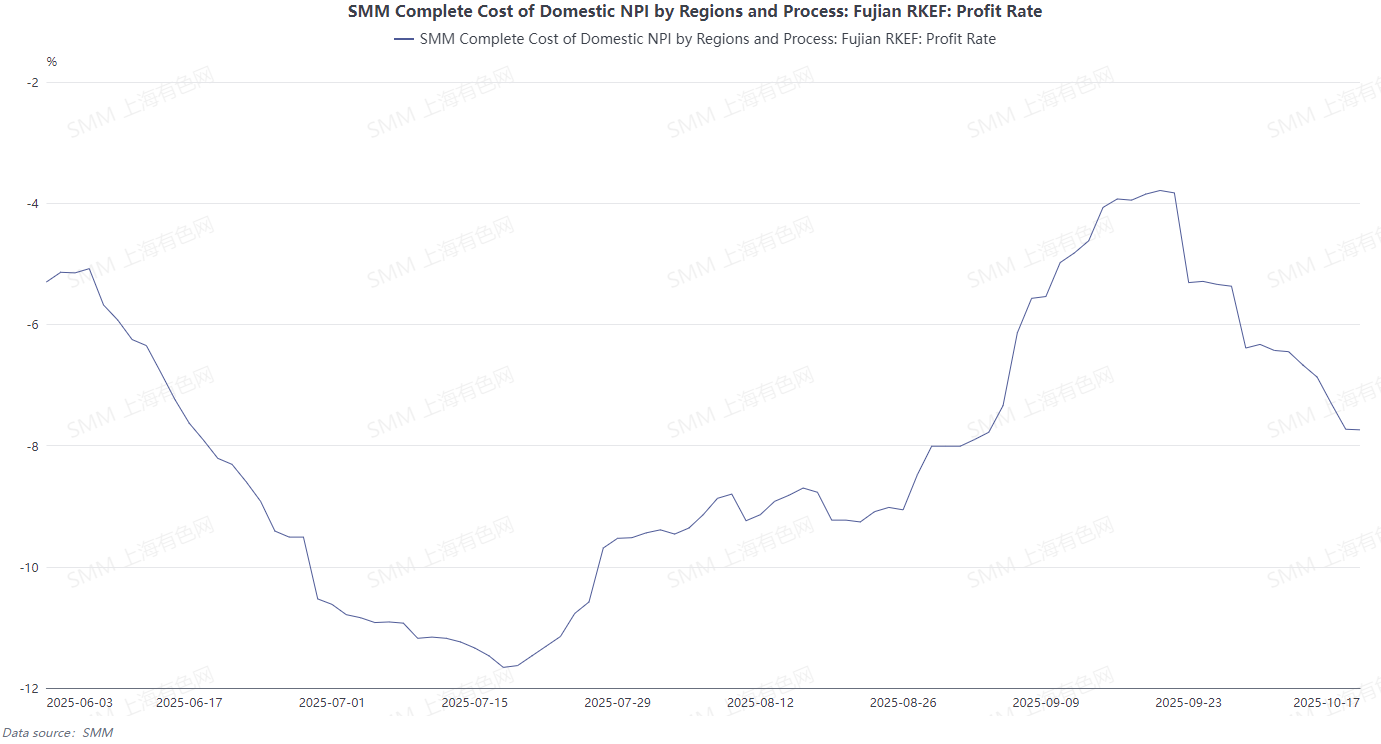

Con base en el costo en efectivo del NPI de alto grado calculado utilizando precios de mineral de hace 25 días, las ganancias de los fundidores de NPI de alto grado continuaron disminuyendo esta semana. En el lado de las materias primas, los precios del mineral de Filipinas e Indonesia se mantuvieron estables, mientras que los precios de los materiales auxiliares continuaron aumentando, impulsando al alza el costo del NPI de alto grado.Al mismo tiempo, la actividad del mercado se mantuvo lenta y los precios del NPI de alto grado continuaron a la baja, ejerciendo mayor presión sobre los beneficios de las fundiciones. De cara a la próxima semana, se espera que los precios del mineral se mantengan firmes, los costes de los materiales auxiliares probablemente permanezcan elevados y se anticipe que los precios del NPI de alto grado sigan bajo presión. Se prevé que las pérdidas de las fundiciones empeoren aún más.

![[Flash de níquel de SMM] Hanrui Cobalt planeó invertir 108 millones de dólares adicionales en su proyecto de mata de níquel](https://imgqn.smm.cn/usercenter/PFIti20251217171734.jpg)